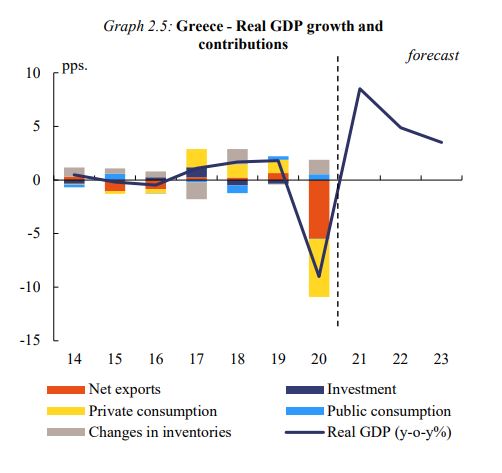

Real GDP in Greece grew by 2.7% (quarter-on-quarter) in 2021-Q3, reflecting strong export performance and a significant contribution from private consumption. The notable recovery in tourist inflows over the summer

helped the economy to reclaim a significant part of the previous losses due to the negative impact of the COVID-19 pandemic, while the industrial sector has rebounded strongly. The recent emergence of the Omicron

variant and the related tightening of containment measures are expected to have weighed on growth in the last quarter of 2021, but its impact is projected to largely fade out during the first quarter of 2022. Overall, real GDP

is expected to have grown 8.5% in 2021.

Growth in 2022 is forecast to be driven by investment, supported by the impetus from the Recovery and Resilience Plan. As consumer spending returns to its pre-pandemic levels, private consumption is also expected to support growth. In addition, the external environment is forecast to remain supportive. Tourism in particular is expected to continue recovering its previous losses, until it fully returns to its pre-pandemic levels by the end of the forecast horizon. Overall, real GDP is projected to grow by 4.9% in 2022 and ease to 3.5% in 2023.

Driven primarily by energy prices, consumer price inflation increased in the last quarter of 2021. Electricity and fuel prices are set to peak during the first quarter of 2022 and ease later in the year. High energy costs are expected to subsequently pass-through to the remaining components of the consumption basket. Headline inflation is forecast at 3.1% in 2022 and 1.1% in 2023. Wage pressures have so far remained limited due to the still large slack in the labour market. The authorities announced an increase in the minimum wage in mid-2022, the size of which will be determined later in the year and therefore is not factored into this forecast.

The risks to the forecast remain elevated. Notwithstanding the quick recovery so far, the evolution of the pandemic represents a source of uncertainty in particular for tourist arrivals. In addition, the projection assumes only a limited negative impact on production from the notable pick-up in input costs. On the upside, the accumulated stock of savings during the pandemic could facilitate a bolder increase in private consumption. The strong performance of goods exports since 2020, could be indicative of structural improvements in the external sector, which could be a source of additional upside risks.